Venezuela is re-engaging with multilateral organizations such as the IMF and the World Bank, largely due to the United States’ strategy to stabilize and boost the economy after January 3rd. Photo: IMF.

Guacamaya, April 17, 2026. The International Monetary Fund and the World Bank are resuming relations with Venezuela after a period of ideological confrontation since 2006 and the non-recognition of these organizations by the government since 2019.

The reestablishment of formal contact comes in a context of internal political changes, the easing of sanctions, and a relative improvement in economic prospects, which coexist with social unrest and political tensions, following January 3, 2026.

For much of the last two decades, the relationship between Venezuela and the IMF has been defined by mistrust, institutional rupture, and a narrative of confrontation. What today appears to be an incipient process of normalization contrasts with a long period of separation that began to consolidate in the early 2000s.

The last formal contact between Venezuelan authorities and the Fund dates back to 2004, within the framework of the Article IV consultations, a standard macroeconomic supervision mechanism. However, after Hugo Chávez came to power in 1999, the relationship began to deteriorate progressively. His government decided to pay off its debts to the IMF and the World Bank early in 2007, thereby cutting ties. It also adopted an openly critical stance, labeling them as instruments of external domination. In 2006, the IMF closed its offices in the country and technical missions ceased.

From then on, Venezuela stopped supplying regular economic information, which severely affected the Fund’s ability to assess its performance. This lack of transparency led the IMF’s Executive Board to issue a censure declaration in 2018 for non-compliance with the statistical obligations established under Article VIII. Since then, the institution has operated practically blind regarding the Venezuelan economy, basing its reports on secondary data and estimates.

In 2019, following the international recognition crisis in Venezuela, the two organizations ceased to consider the government of then-President Nicolás Maduro as the country’s legitimate executive. This decision was made due to disagreement among the main shareholders, which are member states like the U.S. and China.

Special Drawing Rights (SDR)

The institutional distancing also had financial consequences. Although Venezuela maintains an allocation of approximately 3.568 billion Special Drawing Rights (SDR), equivalent to about 5 billion dollars, access to these resources has been blocked due to the lack of international recognition of the government.

The SDR issue has even been addressed in negotiation tables between the government and opposition held in Barbados and Mexico, with Norwegian mediation in previous years, where a Social Fund to address the humanitarian emergency in the country was even discussed.

Without access to multilateral markets, Venezuela turned to bilateral financing, mainly with countries like China and Russia, as well as massive issuances of external debt. This strategy, combined with the economic collapse between 2014 and 2021 — when the country lost more than 70% of its GDP — led to a debt sustainability crisis, currently estimated at around 161 billion dollars.

However, the landscape began to change after the political events of January 3, 2026. With the appointment of Delcy Rodríguez as interim president and the beginning of an institutional reconfiguration process, new windows of opportunity for international re-engagement have opened.

In this context, the IMF recently sent a survey to its member countries to assess their relations with Venezuela, a key step to determine if the necessary consensus exists to recognize the new government. Finally, on April 16, 2026, both the IMF and the World Bank declared that they were resuming formal relations with the Executive led by Delcy Rodríguez.

This shift is influenced by the position of the U.S., the main shareholder of the IMF, with nearly 16% of the voting power. The Trump administration sees the stabilization and economic growth of Venezuela after January 3 as a symbolic victory and an advance for its strategic interests.

Treasury Secretary Scott Bessent has publicly expressed support for Venezuela’s reintegration into the international financial system, stating that the country “is returning to a good trajectory.” This position has materialized in the lifting of sanctions on Venezuela’s public banking system and the issuance of licenses that allow commercial transactions with the government, under supervision.

In parallel, markets have reacted positively, first to the possibility and then to the realization of this re-engagement. Venezuelan dollar-denominated bonds have registered increases, particularly those maturing in 2027 — among the most liquid — which exceeded 48 cents per dollar, reflecting expectations of financial normalization.

From boom to explosion: the history of Venezuela and the IMF between 1946 and 1998.

The relationship between Venezuela and the IMF during the second half of the 20th century underwent a profound transformation, going from being practically irrelevant in times of oil abundance to becoming a central — and highly controversial — factor in the country’s economic and social policy.

Venezuela joined the Fund on December 30, 1946, as a founding member, but for more than three decades maintained a distant relationship. Oil revenue and the strength of the bolivar allowed the country to avoid the cycles of debt and adjustment that marked other Latin American economies. During that period, the link with the IMF was more administrative than operational.

This balance began to crack in the 1980s. The fall in oil prices, increased indebtedness, and capital flight led to the devaluation of the bolivar in 1983, known as “Black Friday.” From then on, Venezuela entered a phase of macroeconomic vulnerability. Although the governments of Luis Herrera Campins and Jaime Lusinchi tried to avoid direct dependence on the Fund, they did so at the cost of international reserves and growing economic distortions.

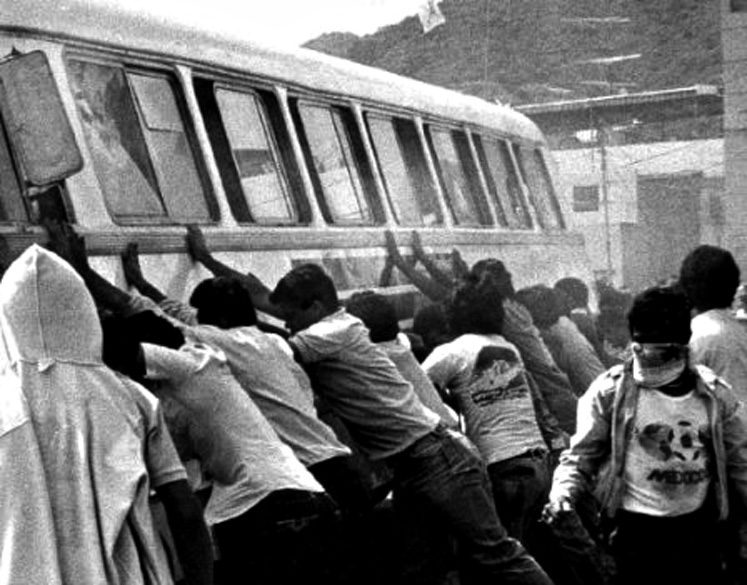

The turning point came in 1989, with the second term of Carlos Andrés Pérez. Facing a collapsed economy — with minimal reserves, high debt, and growing poverty — his government signed a Letter of Intent with the IMF to access financing of around 4.5 billion dollars. In exchange, it adopted a structural adjustment program that included price liberalization, elimination of subsidies, and an increase in the price of gasoline.

These measures, popularly known as “El Paquetazo” (The Package), responded to a logic of macroeconomic stabilization, but their implementation was rapid and socially costly. The fuel increase led to an immediate rise in public transportation prices, triggering protests that began in Guarenas and spread to Caracas and other cities. This became known as “El Caracazo,” which erupted on February 27, 1989, as a reaction to these measures and an accumulated deterioration in living conditions.

The state’s response was massive repression that left hundreds — and according to some estimates, thousands — dead. Beyond its structural causes, the episode consolidated in the collective imagination the idea that the IMF was co-responsible for the adjustment and its social consequences, for having promoted shock policies without sufficient social cushioning.

El Caracazo was a key episode in the narrative of Lieutenant Colonel Hugo Chávez’s political movement, which attempted two coups in 1992. February 27 remains a fundamental element in the Chavista imagination today.

In the following years, the relationship with the Fund continued to be ambivalent. After the 1994 banking crisis, President Rafael Caldera — who had initially rejected the IMF — ended up resorting again to an adjustment program in 1996, known as “Agenda Venezuela.” This included similar reforms aimed at consolidating economic opening, fiscal discipline, and market liberalization, although with a more gradual approach.

However, by the end of the decade, political wear and tear was evident. The perception of loss of economic sovereignty and the social impact of the adjustments fueled a deep rejection of the IMF and the associated economic model. This climate of discontent was key to the collapse of the traditional political system and the rise of Hugo Chávez in 1998, whose narrative was largely built in opposition to “neoliberalism” and the Fund’s role in the Venezuelan crisis.

The reforms proposed by the IMF have also generated massive protests in other countries, even in recent years, such as in Ecuador in 2019, Sudan in 2021, and Ethiopia in 2024. In some cases, popular rejection following other “packages” has led to government changes.

Thus, at the close of the 20th century, the relationship between Venezuela and the IMF was not only deteriorated but also loaded with strong symbolic and political content that would mark the following decades.

The IMF in Venezuela’s new moment: between credibility anchor and political risk

Venezuela’s re-engagement with the IMF occurs at a particularly delicate moment, amidst an incomplete political reform, an incipient economic opening, and an economy that is still deeply fragile. More than a simple institutional return, what is at stake is the role the Fund could play as a stabilization actor, an international signal, and a catalyst for reforms.

For more than two decades, the Venezuelan economy has operated without reliable statistics or international supervision. The Fund itself recognizes that the lack of data limits the accuracy of its diagnoses. A re-engagement — even if technical — allows for reestablishing basic transparency standards covering fiscal data, inflation reserves, an indispensable condition for attracting investment, renegotiating debt, or accessing multilateral financing.

In other words, the IMF is not only a source of resources but, above all, a seal of technical validation for the markets.

A possible bridge to financing and debt restructuring

Venezuela faces one of the highest and most complex debt burdens in the world, which could exceed 150 billion dollars. Without a functional relationship with the IMF, any restructuring process is extremely difficult.

Historically, the Fund has been a central actor in these processes, not only by providing direct financing but also by coordinating with other creditors (Paris Club, multilateral banks, bondholders). In the Venezuelan case, eventual recognition of the government and the resumption of relations could:

- Unlock access to Special Drawing Rights (SDRs).

- Facilitate financial assistance programs.

- Serve as a framework for an orderly future restructuring.

However, this is a medium-term scenario. In the short term, even the current approaches point more towards technical interactions than immediate financing.

A key actor in macroeconomic stabilization

Recent IMF projections reflect a relevant change, indicating growth of 4% in 2026 and 6% in 2027. But this optimism coexists with severe structural risks, including still extremely high inflation, oil dependence, institutional fragility, and exchange rate distortions.

In this context, the Fund could contribute to the design of coherent macroeconomic policies, something that has been absent or fragmented in recent years, focusing on fiscal discipline, a monetary reform leading to exchange rate normalization, and the strengthening of the central bank, the BCV.

However, a central tension appears here: these policies, although technically necessary, can have high social and political costs, as already happened in the past in Venezuela.

The weight of history: legitimacy and political memory

The main limitation of the IMF in Venezuela is not technical, but political and symbolic. The memory of El Caracazo and the adjustment programs of the 1990s remains a determining factor in public perception.

The Fund is associated, in broad sectors, especially within the officialism now led by Delcy Rodríguez after January 3. In the Chavista imagination, key elements persist, such as regressive macro-adjustments, loss of sovereignty, and social crises.

This implies that any role for the IMF today must be handled with extreme care. A stabilization program perceived as “imposed” or socially insensitive could reactivate tensions in a context where social unrest and frustrated expectations already exist, even within Chavismo itself.

An element within a broader architecture

The IMF does not act in a vacuum. Its role must be understood within a broader architecture that today includes the easing of financial sanctions by the U.S., which seeks to reactivate currency flows and banking operations; international energy interest, especially in oil and gas, which now, thanks to various reforms, will have greater private participation; and the possible role of the World Bank and other multilateral actors with an interest in Venezuela.

In this ecosystem, the Fund can function as an articulating piece, but not as the sole solution. Venezuelan stabilization will depend as much on external factors (oil prices, geopolitics) as on internal matters (governability, reforms, and social cohesion, key for stability).

Between opportunity and risk

In neutral terms, the IMF today represents three things simultaneously for Venezuela:

- An opportunity: to regain access to financing, credibility, and economic governance.

- A technical tool: to bring order to a deeply distorted economy.

- A political risk: due to its historical baggage and the potential social cost of its recommendations.

The central challenge will be whether Venezuela manages to integrate the Fund into a gradual, politically viable, and socially sustainable stabilization process, avoiding repeating the mistakes of the 1990s.

The World Bank resumes relations with Venezuela after a seven-year pause

A few hours after the IMF’s announcement, it was learned through an official statement that ties between Venezuela and the World Bank had been reestablished, marking a new chapter in a relationship historically more technical than political, but equally affected by the country’s cycles of boom, crisis, and confrontation with the international financial system.

Unlike the International Monetary Fund — more associated with macroeconomic stabilization — the World Bank has traditionally had a role focused on financing development projects, infrastructure, and social policies. Venezuela was part of this scheme from the mid-20th century, benefiting from loans aimed at public works, energy, and institutional modernization, in line with the organization’s mandate since its creation at Bretton Woods.

During the years of the oil boom, however, the link was limited. The country did not depend structurally on this type of financing and, at times, even adopted a position of autonomy vis-à-vis the organization. An illustrative episode occurred in 1984, when the government of Jaime Lusinchi withdrew deposits from the World Bank following the rejection of a key loan for hydroelectric development, reflecting early tensions in the relationship.

In the 1990s and early 2000s, the World Bank maintained a certain presence in the country through specific projects and technical cooperation. However, this relationship began to weaken progressively during Hugo Chávez’s government, in parallel with the deterioration with other multilateral organizations. By 2005, a significant reduction in the project portfolio and internal questioning about the continuity of the relationship were already evident.

The distancing deepened in the following decade, amidst sanctions, political disputes, and growing international isolation. In practice, the World Bank ceased to have an active loan portfolio in Venezuela, reflecting almost total operational disconnection in recent years.

The seven-year pause in relations — now reversed — must be understood in this broader context of financial isolation and institutional rupture. Its resumption, as in the case of the IMF, responds both to recent political changes and to a reconfiguration of the international environment towards Venezuela.

The return of the World Bank could have concrete implications in critical areas such as infrastructure and public services (electricity, water, and transport), which are three key elements for any recovery and include: Social programs and poverty reduction, institutional strengthening and governance, and technical assistance for economic reforms.

Unlike the IMF, whose intervention is usually associated with adjustment programs, the World Bank can offer a more gradual and sectoral approach, making it a potentially key actor in a phase of economic reconstruction.

Elías Ferrer collaborated in the writing of this article.